Key points

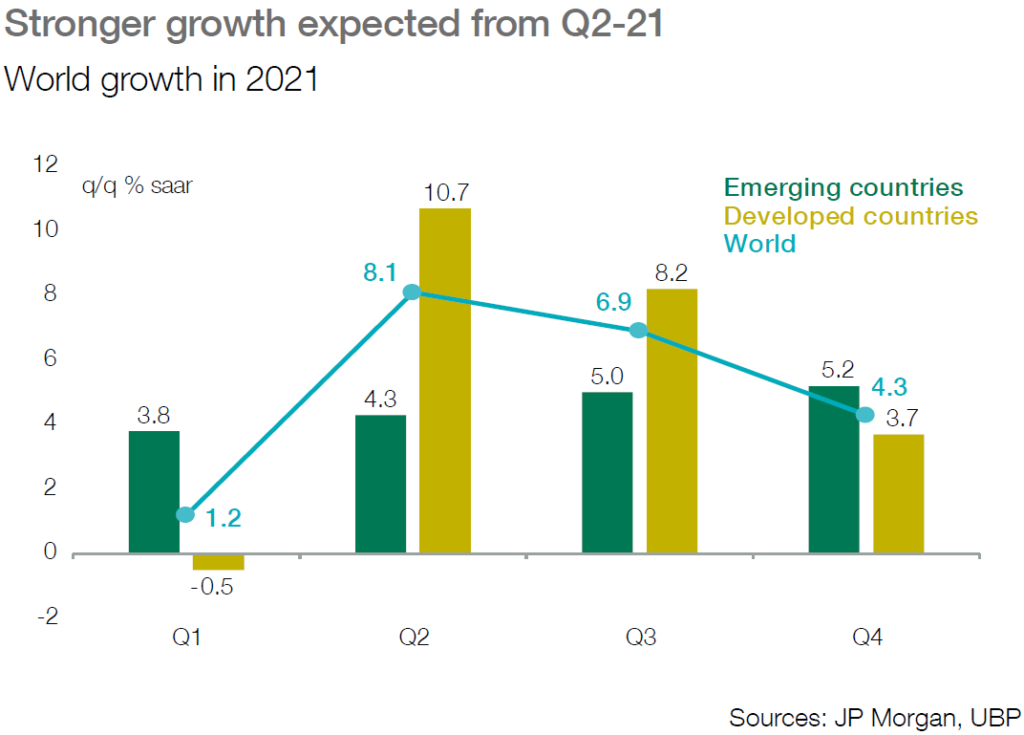

■ Activity remained weak in Q1-21, still dominated by new variants and lockdowns; Q2-21 is expected to be a turning point for both the pandemic and economic activity thanks to a rising share of the global population being vaccinated.

■ Government reflation policy is working and the reopening of economies expected from Q2 should lead to a strong growth momentum and prospects of a synchronised rebound in H2-21.

■ The budgetary support should favour consumers and restore investment; monetary policy will remain accommodative but progressively more vigilant on inflation.

US growth to accelerate after weak start

■ Bad weather conditions, a volatile labour market and a virus which was still active were responsible for moderate growth in Q1, but thanks to the accelerating vaccination rollout a strong rebound is expected from Q2-21.

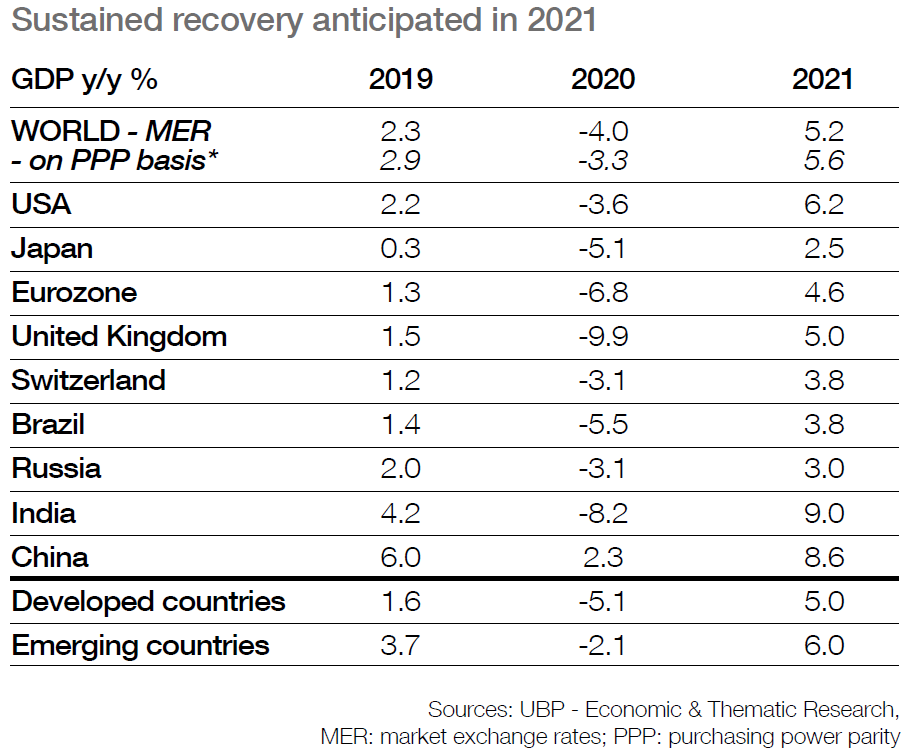

■ The USD 1.9 tr package should come into efect rapidly, with less opposition than feared. Biden’s administration is on track to present a new investment plan based on climate change, environment and innovative technologies.

UK to reopen soon, while eurozone is still lagging

■ After being penalised by Brexit and high levels of Covid infections, the UK should benefit from its rapid and widespread vaccination campaign. After a depressed Q1, reopening should boost activity from Q2, with growth set to recover by 5% in 2021.

■ In the eurozone, slow vaccination rollouts mean lockdowns remain in place. Growth entered a double dip recession and stayed depressed in Q1, but manufacturing was resilient; a strong Q2 rebound is expected.

Ongoing recovery in Asia

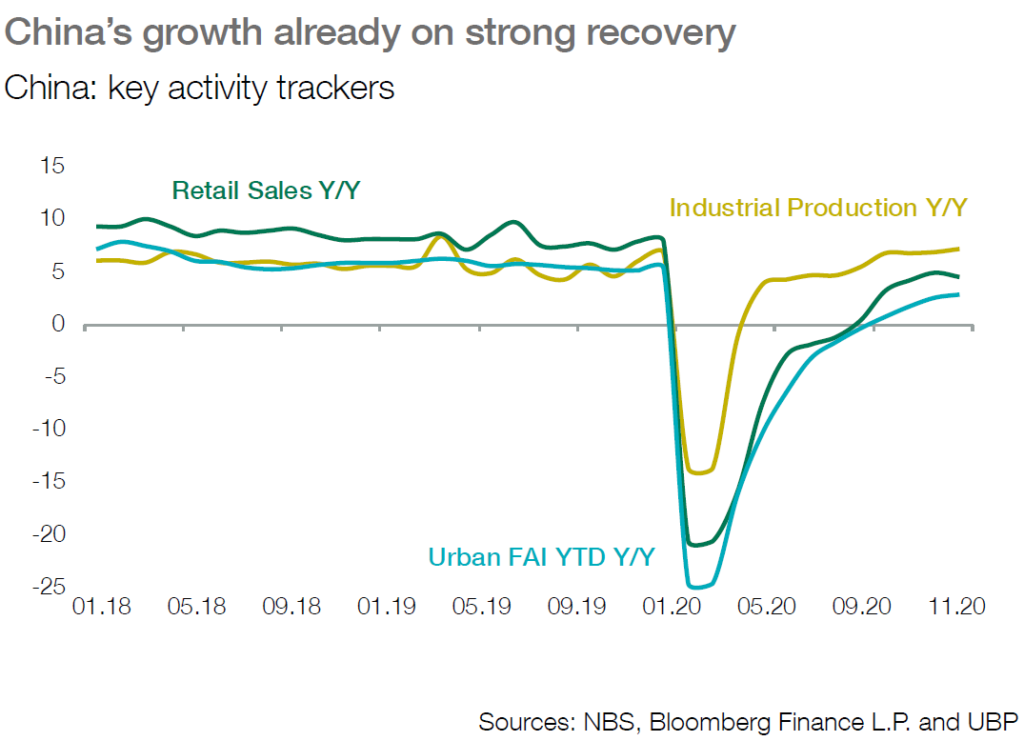

■ In Asia, activity has regained some vigour but headwinds appeared due to shortages in transport and IT sectors. A sustained recovery is expected thanks to domestic demand and renewed budgetary supports.

■ In China, exports and investment recovered but restrictions on travel weighed down on consumption during Lunar New Year. A stronger growth profile looks likely as economic policy favours consumption, local innovation and investment.